Lately, YouTube is full of videos that predict the imminent collapse of China’s real estate. Some extrapolate it to the entire Chinese economy and make ridiculous claims like “China’s economy will collapse in 30 days.” Not surprisingly, these videos get millions of views. Americans love doom-and-gloom narratives about China.

But here are three reasons why China’s real estate is not going to collapse in the next month or the next year or anytime in the near future.

**1. Most Chinese fully own their homes — i.e., they don’t have any mortgage.

According to this 2016 Forbes article, 80% of Chinese homeowners have no mortgage — they own the homes outright! That number may be a bit smaller now, since home prices have gone up a lot since then, but the it is still astonishingly high. Thus, such people are not going to sell their homes even if the prices go down dramatically. It’s just theoretical loss and doesn’t affect their lives. So,

According to this 2016 Forbes article, 80% of Chinese homeowners have no mortgage — they own the homes outright! That number may be a bit smaller now, since home prices have gone up a lot since then, but the it is still astonishingly high. Thus, such people are not going to sell their homes even if the prices go down dramatically. It’s just theoretical loss and doesn’t affect their lives.

In summary, there won’t be any panic selling of homes; and there won’t be any foreclosure crisis regarding banks (like it happened in the US during the 2008 mortgage crisis).

**2. New buyers will stop any downward trend

As prices go down, housing will attract new buyers. There are many young people who can’t afford homes right now. For them, houses will become more affordable if prices go down, say, 20%. There will also be speculators who will come back when the home prices start to drop.

Finally, the government can also buy homes as they get cheaper. And it’s being done already. For example, state-owned enterprises (SOE) are buying apartments and renting them out to low-income residents at rates below the market rate. Solve the real estate problem and help the poor at the same time! Win-win.

Thus, increased demand from new buyers — individuals and the government — will stop any downward spiral of housing prices.

(By the way, the rich people and the speculators have multiple homes in China. If the housing bubble pops, these are the people who will sell their investment homes at losses. And they can afford it).

**3. Government has plenty of tools

The Chinese system is very different from the Western economies. This is why China has not had a single recession or a financial crisis in 40 years. Everyone gets together and coordinates their actions — central government, local governments, state-owned enterprises, banks, real estate developers, giant corporate conglomerates etc. all pitch in and work together.

Consider the mortgage boycotts, which got a lot of attention in the Western social media. Well, Evergrande and other developers have now gotten special loans to restart the unfinished real estate projects within a month. And because it’s China, the government can also force these developers to finish the projects on time. One advantage of an authoritarian system!

There are countless other tools for the government. For example: Decreasing mortgage rates, lowering down payments, setting price controls (“price should be at least so many Yuan per square foot”), subsidies for young and married couple to buy homes, and so on. There is no market ideology in China, so any pragmatic idea will be quickly adopted.

Current Situation

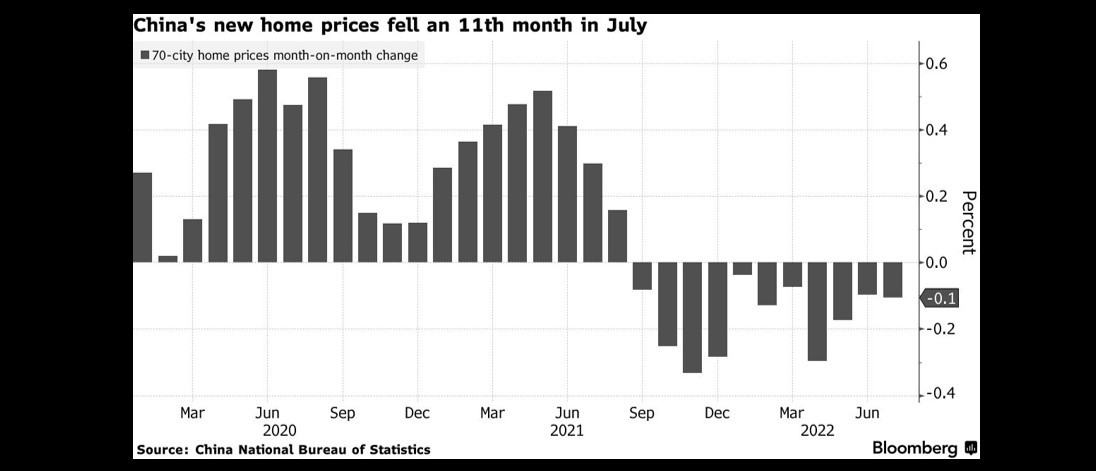

While property sales across China have plunged 30% and prices have declined 11 months in a row, here is the good news: Overall prices are down only 3% over the last year. In big cities like Beijing, Shenzhen and Shanghai, prices are actually edging up a bit. That’s a stable situation — and it’s more like a controlled deflation of the housing bubble.

Conclusion

The real estate bubble in China is real. Prices in Tier 1 cities are astronomical. This is why the government pricked the bubble two years ago with new rules about debts for property developers. The first goal is to make housing more affordable; the bigger goal is a fundamental shift in China’s economy, reducing dependence on real estate and construction as tools to generate growth. Of course, this is a gradual process and cannot be done overnight.

Over the next decade or so, China’s real estate sector will likely stagnate as the workforce population shrinks every year. However, there won’t be any “collapse.”

(I can even think of another creative way to stimulate China’s real estate sector in a decade: Move people away from high-rise buildings to individual homes. It will stimulate the economy and make cities more appealing).

Finally and more importantly, China is on the cusp of becoming a true global power. With careful stewardship, China will surpass the US and become the #1 economy within 5 years or so. After being kept down for 200 years, China finally has a chance to rise again. The leaders and the people are not going to squander this rare and great opportunity just because there are some problems with real estate. That’s too silly.