It’s never fun to warn people about an imminent crisis, especially at peak euphoria. Trump and his voters constantly boast about the economy and the stock market and, of course, Obama and his fans did the same during his tenure. This reflects a fundamental misunderstanding about the driving factors behind the deceptively good numbers since the last financial crisis. Let’s deconstruct the fake news about the fake economy.

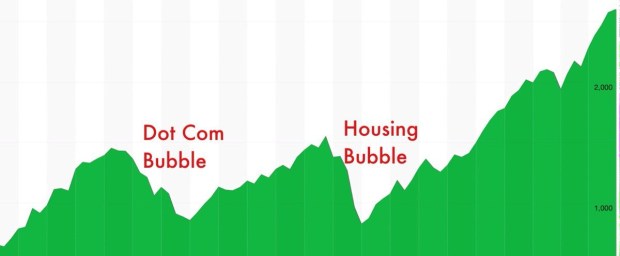

Let’s start with the start market. Does this chart of S&P 500 index like a bubble? That’s 250% growth in 8 years!

Since all the Central Banks around the world are linked, the Global Dow has also tripled in the same interval:

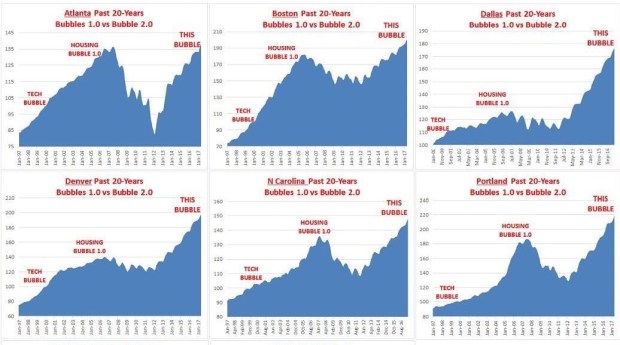

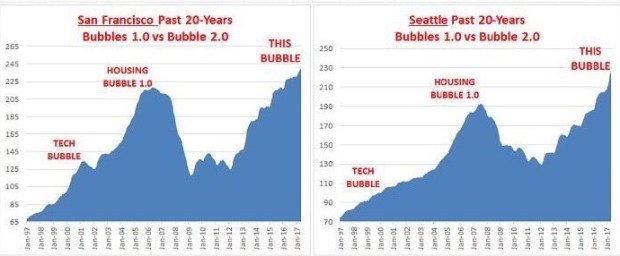

Not having learned the lesson from the housing bubble that crashed the global economy, the elites have created a sequel. Here’s the Case Schiller Index for various cities in the US. Do they seem frothy?

Around the world, there are massive real estate bubbles in Canada, Australia, UK etc. (Since the global economies are all linked, you should care). And Sweden tops them all:

Then there is a new asset bubble: auto loans, which is up 50%, even though Americans haven’t gotten 50% wealthier.

Another debt bubble that has reached insanity is the student loan, which now stands at $1.4 trillion (doubled since 2009). The student loan was a desperate scheme by the government to reduce the official unemployment rate after the economy tanked in 2008.

The US non-financial corporate debt ($8.7 trillion, amounting to 45% of GDP) and household debt ($13 trillion) are also at record levels. Chart below shows the rise of US credit card debt:

The federal government has doubled its debt since 2008 and the debt-to-GDP has gone from under 70% to more than 100%:

Three Types of Bubbles: Bad, Worse and Ugly

Bubbles are always bad because they are illogical and, when they burst, cause a lot of pain. A bubble depends on the “greater fool theory,” whereby each person hopes that there will be a bigger idiot who will pay even more for an asset. Bubbles also appeal to the get-rich-quick fantasy.

There are three different types of bubbles.

Irrational Bubble: This is the simplest one that’s caused by hype, herd mentality and greed. Without any change in the fundamentals, the price of a product keeps going up. Whether it’s the Tulip Mania of the 17th century or the BitCoin bubble of the 21st century, the principle driving the irrational exuberance is the same: human psychology.

Debt-driven Bubble: This is worse than a simple bubble, since people get into debts, hoping for a massive return. Mortgage, of course, is the biggest debt for most people. American middle class lost 40% of their wealth after the great financial crisis of 2008, but they forgot all about it a few years later. When the bubble bursts, everyone – families, corporations and governments – are left deeper in the hole (except for the few lucky ones and insiders who make it like bandits).

Bubble Fueled by Debt, Money-Printing and Loose Standards: This is akin to that bartender who seems to have a lot of energy. Then you find out that he had coffee at 9 pm, Redbull at 10 pm, Ecstasy pills at 11, cocaine at midnight and meth at 2 am. The current bubble is fueled by money-printing by the central banks, artificially low interest rates set by the central banks, and loose standards for loans.

Since the 2008 crisis, the big central banks in the U.S., EU and Japan – Fed, ECB and BOJ respectively – have (digitally) printed more than $10 trillion out of thin air. Then the commercial banks turned them into $100 trillion or more, thanks to the fractional reserve system.

The Fed and other central banks also coordinated and synchronized their actions (this is the essence of “One World Government”) and reduced the prime interest rates to virtually zero (“ZIRP” policy) and held it there for 8 years.

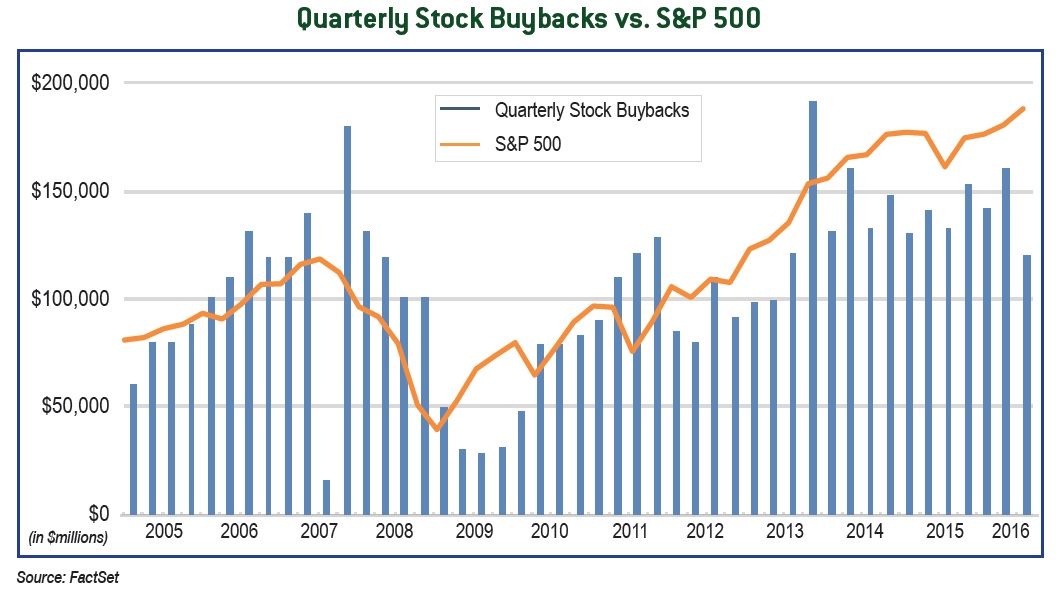

Easy money meant that big corporations spent trillions of dollars – including massive debts – to buy back their own shares. The ECB has spent billions buying corporate bonds and the BOJ has spent billions buying stocks. Of course, the stock market has tripled.

Chart below shows stock buybacks by US corporations:

Financial engineering also created Housing Bubble 2.0 and other newer bubbles. Keep slashing the required down payments, incomes and credit scores, you will get more new buyers for more expensive homes and cars. Creating a bubble is not rocket science.

Wealth versus Wealth-Effect: Somewhere along the way, we collectively lost the notion of what true wealth is. Earning and saving have been replaced by borrowing, spending and speculating. In this environment, the entire nation has turned into Las Vegas, and Casino Capitalism has become the norm.

Disregard for Fundamentals: Since 2008, the US GDP grew by 35% while the stock market grew by 250%. Does that sound reasonable? Tesla has lost more than $3 billion in the last five years, but its stock price went up 10-fold during the same time. If you invested money in Amazon shares, it will take 250 years to get your money back through its earnings. Australia’s housing market is 4 times its GDP. There’s no logic when the society is caught up in a frenzy.

What’s Next?

This time is not different. All we have done since 2008 is rinse and repeat. We replaced the housing bubble with Everything Bubble. The bubbles will soon start popping all over the world (except for a few countries like Russia that has very low debt). The timing depends on how fast and how much the central banks will raise the interest rates. Even a 2% point rate hike is enough to pop the bubble, since bond markets, housing and stock buybacks are all very sensitive to interest rates. However, even without the interest rate hikes, the debt binge is coming to an end, as households and corporations are close to being maxed out. When there are no more new buyers, there will be a stampede towards the exit door. 2018 might very well turn out to be the year when the house of cards collapses again.

(Originally published on Activist Post)

Author: Chris Kanthan Check out Syria – War of Deception, my new e-book on the Syrian war, the most consequential war of recent times

{kind=link}