The financial struggles of China’s real estate developers have been making the headlines for the last few months. There are two lines of thoughts on this crisis. First, China’s real estate bubble is bursting like what the U.S. experienced in 2008. Second, this is no big deal or even this is a good thing for China’s economy, since it will make housing more affordable. Both these notions are wrong. Let’s see why.

Outsized Role of Real Estate

China’s real estate is a critical pillar of China’s economy, unlike any other country. Consider these four stats on how much China’s real estate accounts for:

- 30% of China’s GDP

- 40% of bank loans

- 50% of fiscal revenues of local governments

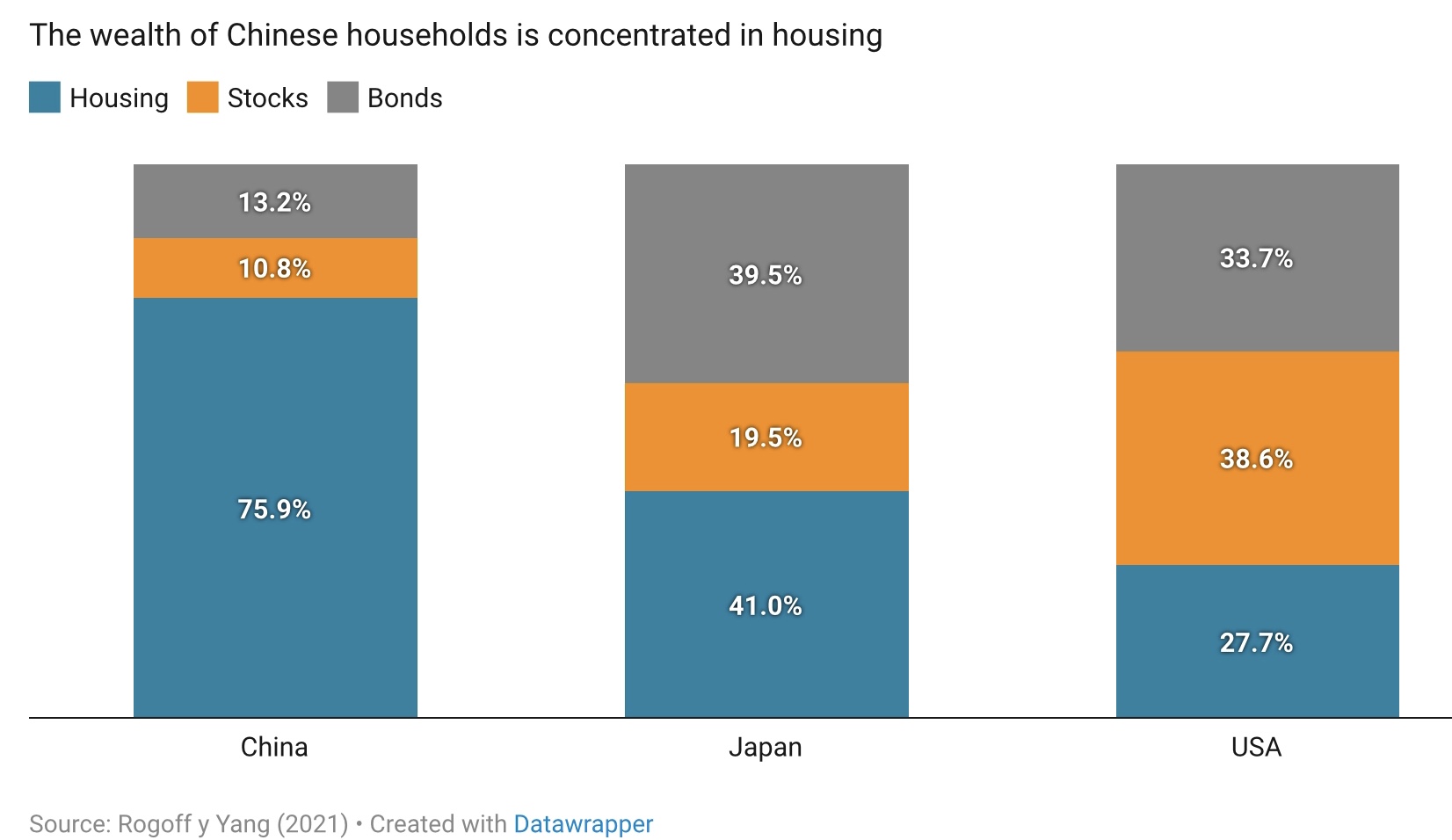

- 75% of household wealth

Why Real Estate Cannot be Easily Deflated

Those are incredible numbers. For example, even during the height of America’s housing bubble, real estate accounted for only 18% of U.S. GDP.

If China’s real estate stalls for a year, China’s GDP growth will be, for example, 4.2% rather than 6%. Bank of America analysts calculate that if home prices fall 10%, China’s GDP growth rate could be as low as 2.2% next year.

Chinese real estate developers depend on pre-sales of new apartments to finish the construction of older apartments. This is like a Ponzi scheme but has become popular in China. People often pay upfront the full cost of a home and then wait for 2-3 years for the home to be built.

Property behemoth Evergrande is a poster-child of this problem. It has 800+ properties and 1.4 million apartments under development in 200+ cities in China. Now, Evergrande is running out of cash and funding (from banks, trusts, and bond markets). The property giant is facing $300 billion of debt and liabilities, making it the most-indebted developer in the world.

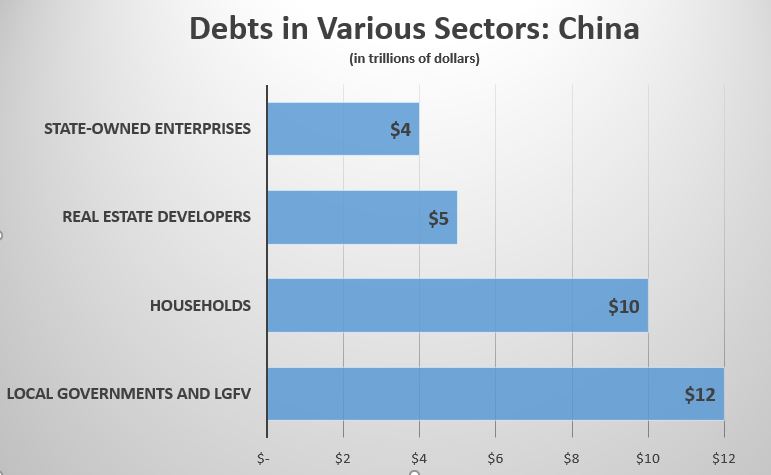

Evergrande is not an exception. Combined, real estate developers in China have whopping $5.2 TRILLION of debt. If home prices plunge and property developers go bankrupt, Chinese banks will be left with bad loans worth trillions of dollars.

As for local governments, they won’t have enough money for infrastructure, schools, healthcare, pensions etc. without revenue from land sales to developers. Some are starting to implement property tax but there is a lot of opposition from existing homeowners.

And considering that 75% of Chinese families’ wealth is tied up in real estate (i.e., homes), the government cannot afford to let home prices go down too much. Also, the top 10% in China have most of this wealth — they own three or more homes — and they are the upper middle class that even Xi Jinping cannot alienate.

There is also another important consideration: jobs. 50 million people work in construction alone. Add in the upstream and downstream jobs like in cement, steel, appliances (refrigerators, ovens, washing machines and so on), furniture, lighting, real estate agents etc., more than 100 million jobs are dependent on the real estate market.

So, everyone is too reliant on the health of the real estate market — the central government, local governments, developers, homeowners, manufacturers and more. Thus, Xi Jinping and his bureaucrats will do whatever it takes to ensure that the bubble doesn’t burst spectacularly. And the Chinese government has tools like price controls, money-printing, rolling over loans etc. to avoid an immediate collapse.

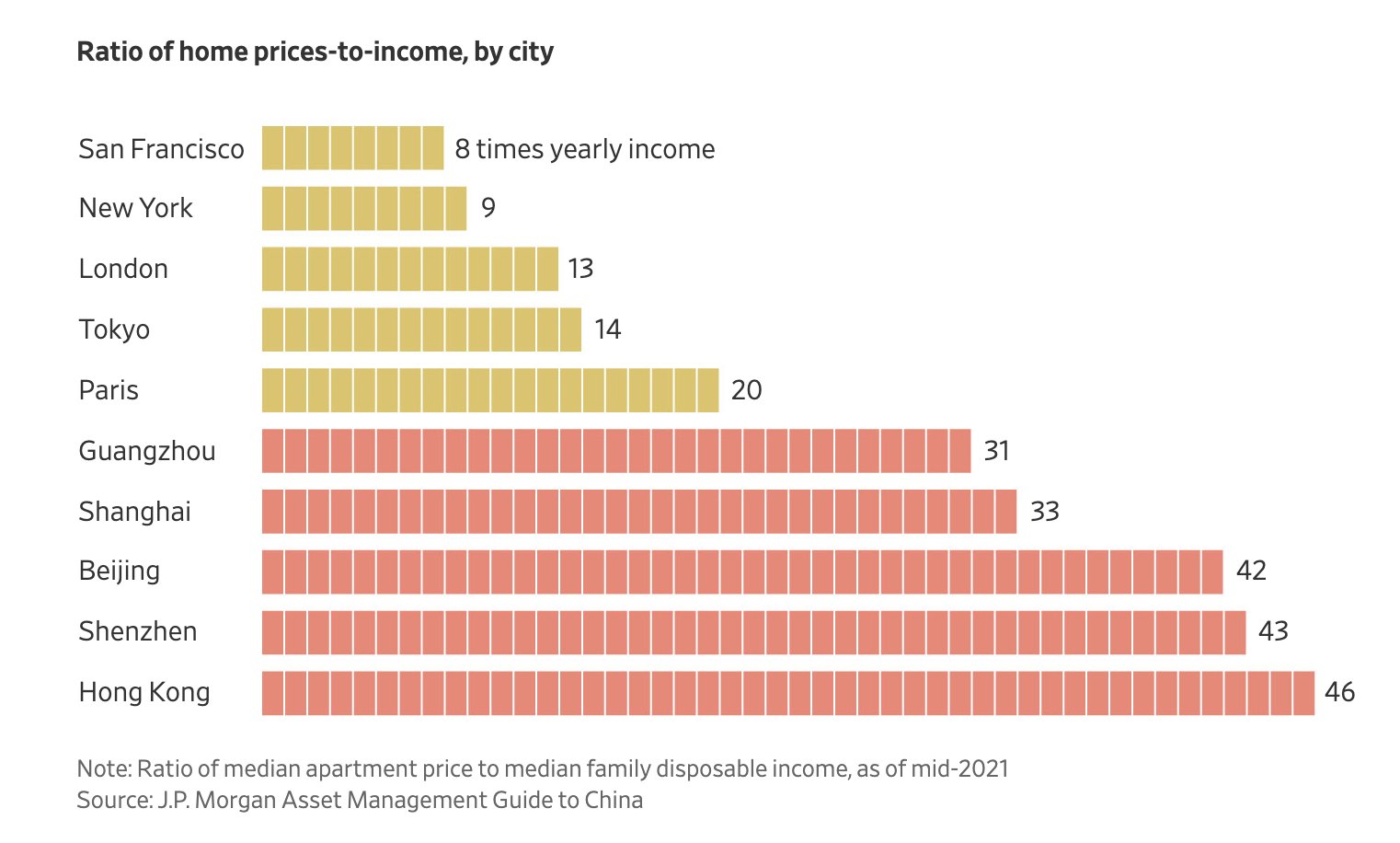

However, maintaining the bubble, of course, means housing will remain unaffordable for most urban young people and all migrants (Chinese people who moved from rural provinces to cities). For example, apartments in Shanghai cost about $700 per square foot — that’s the same as New York City or San Francisco. However, the average after-tax income in Shanghai is only $1000 a month.

Looking at the ratio of median house price to median annual income, Chinese cities are fivefold more expensive than Western cities like New York City or San Francisco.

If China wants to make housing affordable, the prices of homes have to come down by 50% or so. But that would devastate the economy. Thus Xi Jinping’s promise to reduce inequality and bring in “common prosperity” will remain a sham.

Long-term Stagnation is Unavoidable

The only real option for the Chinese government is to kick the can down the road. They should have pricked the housing bubble six years ago when there was a slump. Instead the CCP panicked and bailed out the real estate sector.

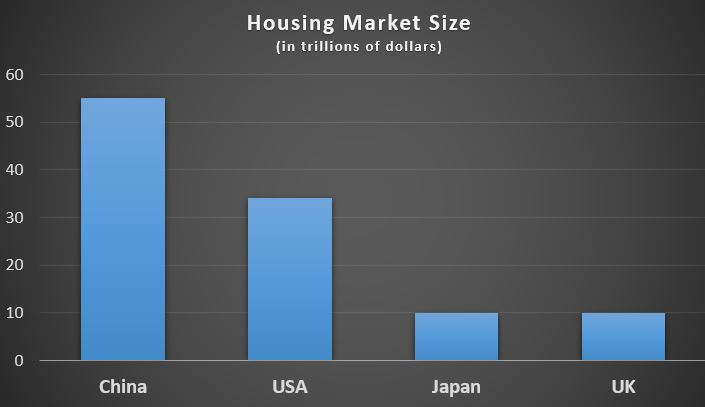

Now the bubble has become the biggest asset class in the world, worth staggering $55 trillion.

Worse, there are 100 million or so vacant and unfinished apartments in China. The much-heralded technocrats in China are supposed to be visionaries who planned decades ahead, but they terribly mismanaged this crucial pillar of the economy.

The housing mania has also led to extraordinary and unsustainable debt for households, developers, local governments, and state-owned enterprises. Deleveraging all this debt will be mission impossible.

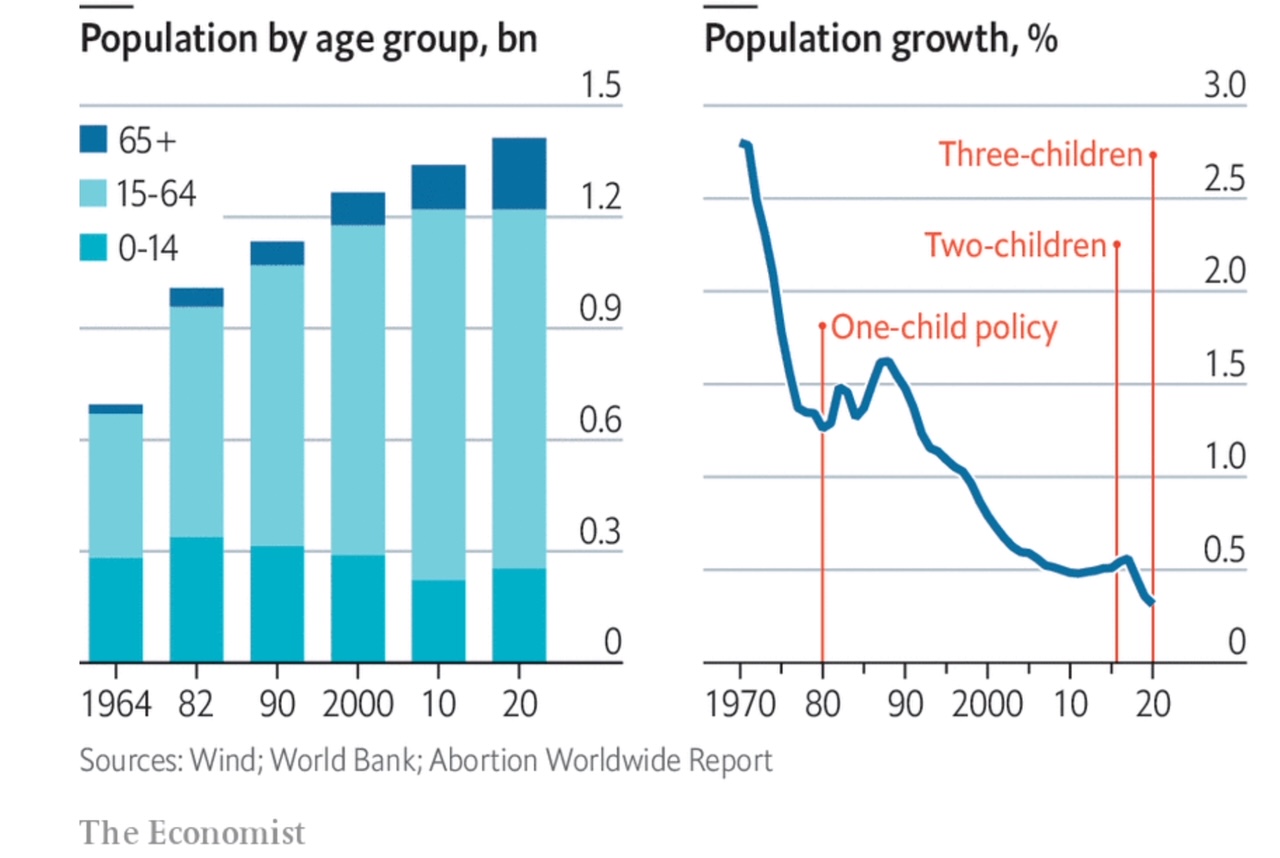

In addition to pure math and finance, the real estate sector faces another dreadful blow: China’s demographic crisis. The prime-age, home-buyer population (25-40) has already been shrinking for the last few years.

There is no reversing this trend. In fact, every stat for demographics is terrible for China: labor force is shrinking, marriage rate is down 40% in the last 8 years, birth rate and fertility rate (1.3) have plunged, and the population of retired people is rising rapidly (already at 300 million).

The future for China’s real estate sector will be like what Japan experienced in the 1990s — prolonged stagnation and a slow, painful death.

The smart Chinese will realize that the real estate boom is over and will start selling their second and third homes discretely. A 3% return from government bonds will be better than losing 20% in real estate.

-Chris Kanthan, author of China, China, Chyyna – Greatest Disruption to American Century